Just earlier in April last year, local headlines were dominated by news about soaring rents in Singapore, putting the spotlight on the declining affordability of tenants and fuelling discussions about an overheated rental market.

However, that story has since lost much of its relevance. Due to the easing of factors which contributed to cost pressures in the past, such as construction delays and pandemic-driven demand, the rental growth of residential properties has softened.

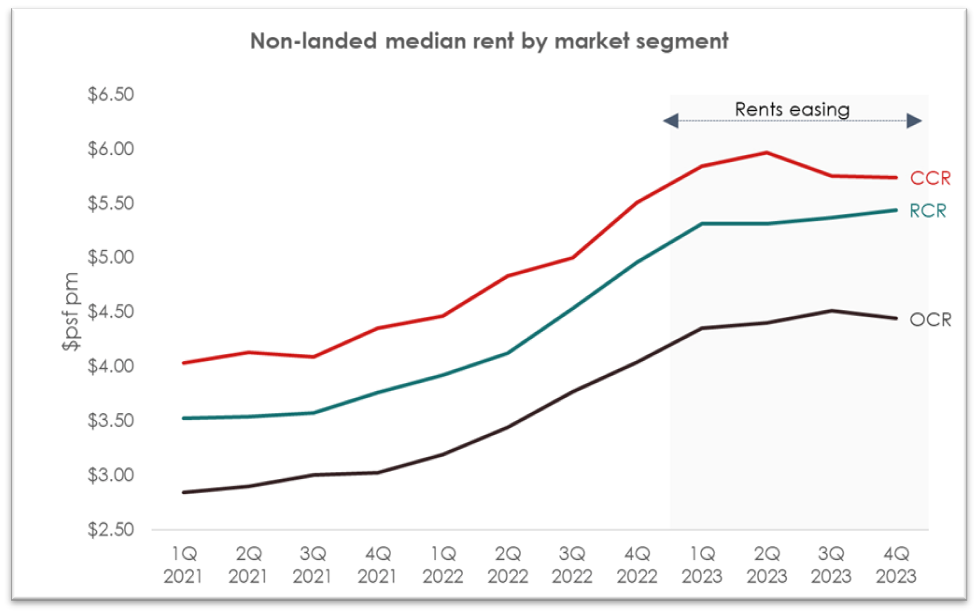

Since the first quarter of 2023, median rents for non-landed private properties across Singapore have grown at a pace that is more moderate.

Private home rents in Singapore saw a significant climb in 2022, rising by 27.9% across the year after a 9.9% increase in 2021. However, for the entirety of 2023, a much slower pace of growth was recorded at 8.7%.

This is good news for tenants as the momentum of rent increases has slowed, which likely means less pressure on their pockets down the road.

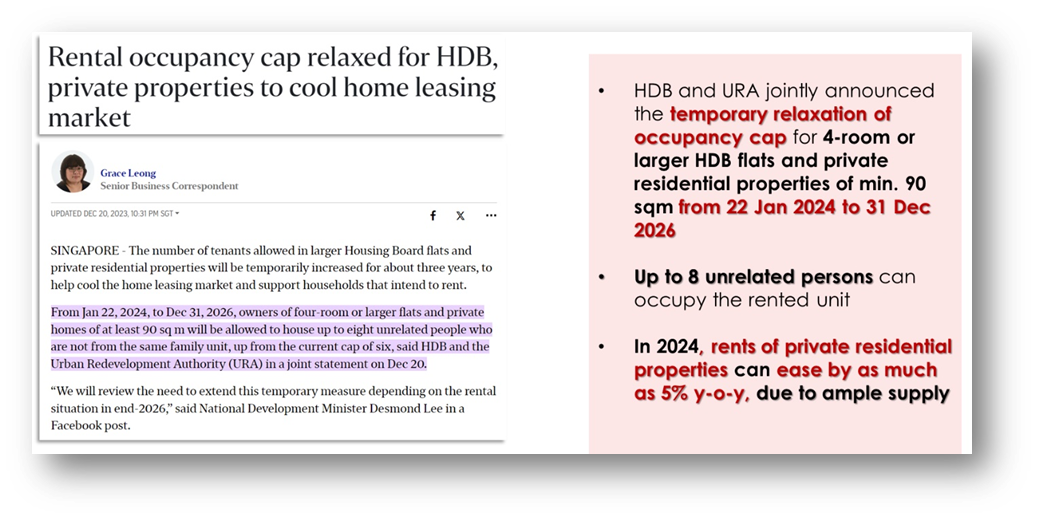

Aside from the uptick in non-landed private properties achieving their TOP – estimated to be 19,000 units in 2023 and a further 9,800-odd units in 2024 – the recent relaxation of occupancy caps for HDB and private homes could also play a role in easing pressure on residential rents.

From 22 Jan 2024 to 31 Dec 2026, up to eight unrelated persons can occupy rented 4-room or larger HDB flats, as well as private residential properties that are at least 90 sqm in size.

By providing breathing room for Singapore’s housing supply to catch up, this temporary change will not only contribute to stabilising the rental market, but also offer hope of more affordable housing for tenants.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers.

For avoidance of doubt, ERA Realty Network and its salespersons accept no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.