Economic Overview

Singapore’s economy further expanded by 3.8% year-on-year (y-o-y) in 1Q 2025, an increase from the 4.4% growth in 2024. However, on a quarter-on-quarter (q-o-q) basis, Singapore’s Gross Domestic Product (GDP) contracted by 0.8%. Among the sectors, the ‘Information & Communications, Finance & Insurance and Professional Services’ and the ‘Manufacturing’ Sector posted the sharpest GDP declines, contracting by 5.0% and 4.9% q-o-q respectively in 1Q 2025.

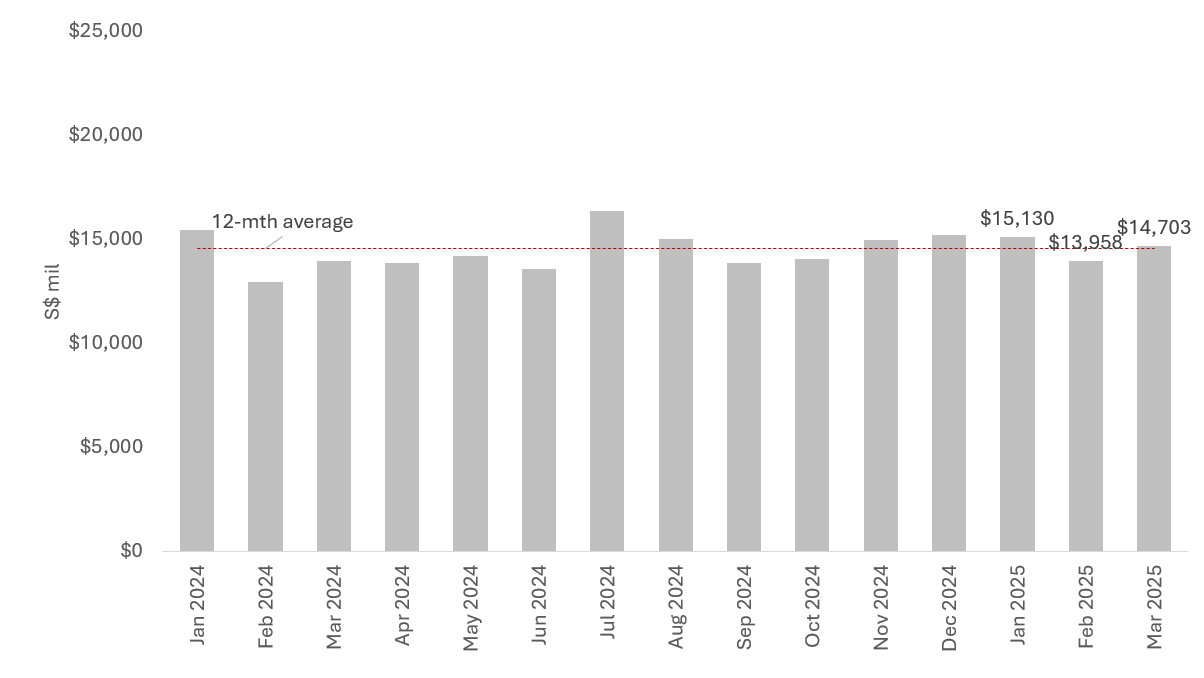

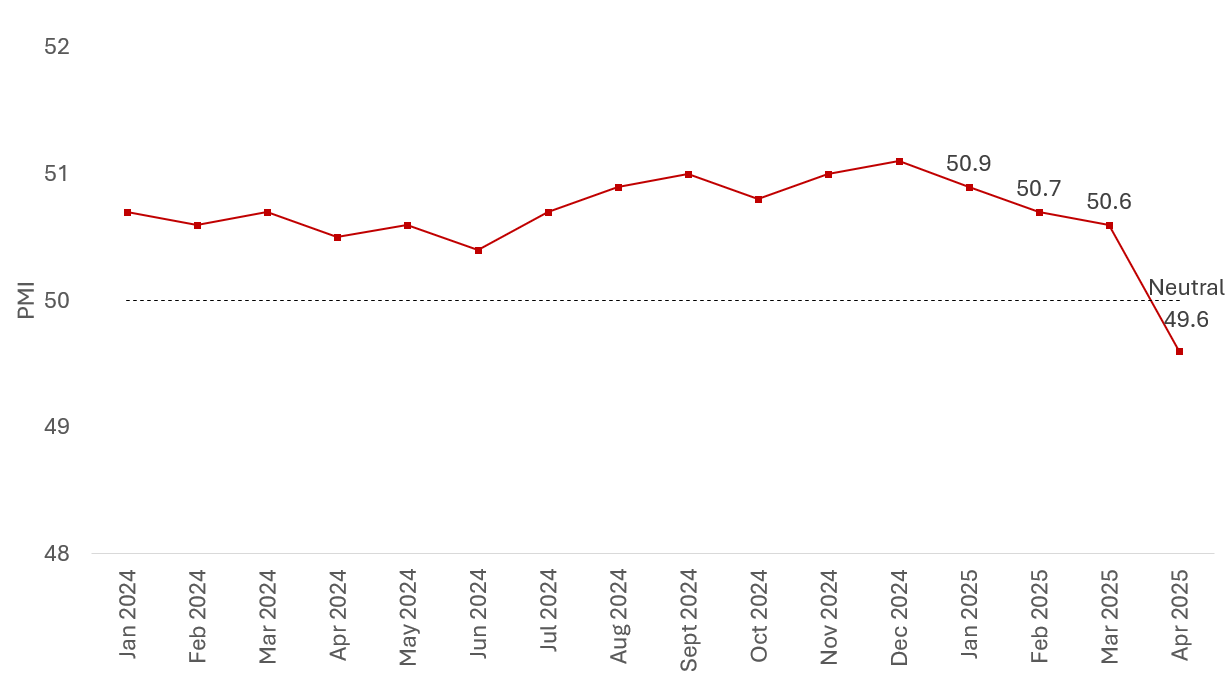

On a more positive note, Non-Oil Domestic Exports (NODX) remained above the previous 12-month average in January and March 2025, with only February registering a dip below the average. In the same vein, the Purchasing Manager Index (PMI) continued to indicate expansion, although it showed signs of gradual moderation over the first three months of 2025, with April’s PMI index dropping to under 50, ending a 19-month streak of expansion.

Chart 1: Non-Oil Domestic Exports and Manufacturing Exports

Source: Singstat, ERA Research and Market Intelligence

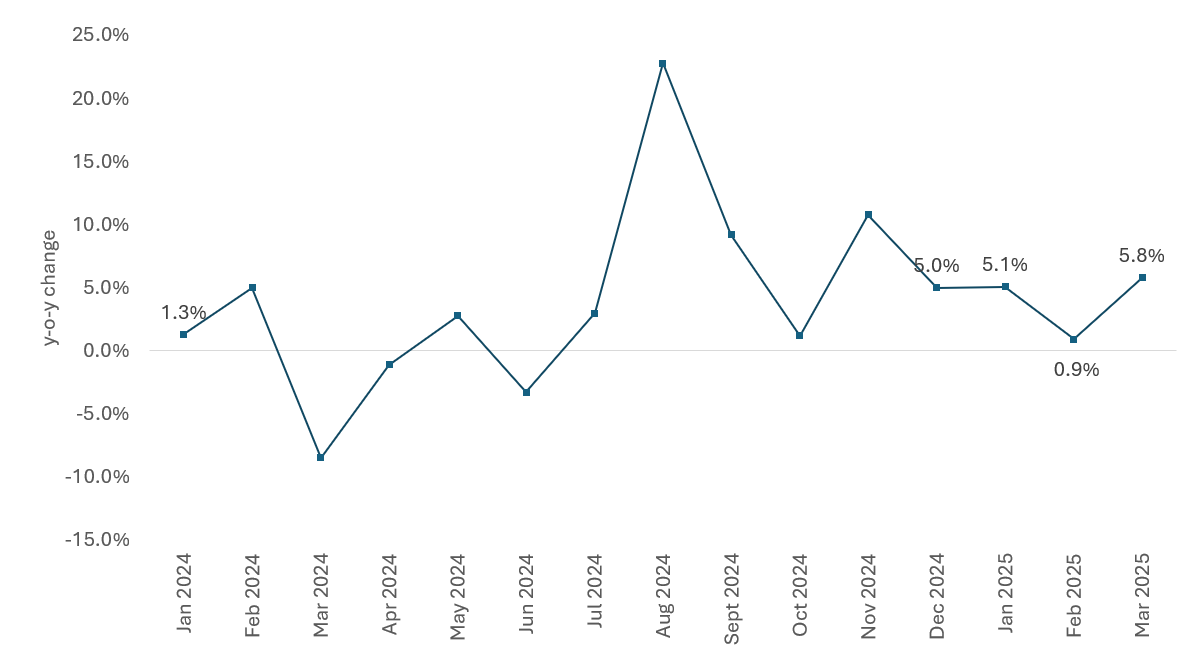

Chart 2: Manufacturing Output y-o-y Change

Source: Singstat, ERA Research and Market Intelligence

Chart 3: Purchasing Manager Index

Source: SIPMM, ERA Research and Market Intelligence

*The PMI reading with a score above 50 indicates that the manufacturing economy is generally expanding and that the economy is generally declining when the reading falls below 50, and a score of 50 indicates no change from the previous month.

Trump’s Tariffs Raises Uncertainty

US President Donald Trump’s unpredictable trade policy has instilled fear and uncertainty in financial markets. Singapore was viewed as an early “beneficiary,” as it faced the baseline 10% tariffs, the lowest among Asian countries. Firms seeking to mitigate risks in their supply chains from countries with higher rates may consider relocating or expanding production in Singapore.

However, Trump has since paused the tariffs for 90 days (from April 9, 2025) and capped all countries’ rates at the baseline 10%, except for China, Mexico, and Canada.

These fluid and ever-changing circumstances will keep firms on the sidelines. What happens after the 90 days remains to be seen. Trade partners could introduce retaliatory actions that may potentially intensify trade tensions. This could impact not just manufacturing, but also the demand for logistics and industrial services, as well as space and labour.

In light of the ongoing headwinds, the Monetary Authority of Singapore (MAS) has lowered Singapore’s 2025 GDP growth forecast to a range of 0.0–2.0% due to heightened geopolitical challenges. As a result, business confidence regarding future expansion is expected to be more measured, with firms likely adopting a cautiously optimistic stance.

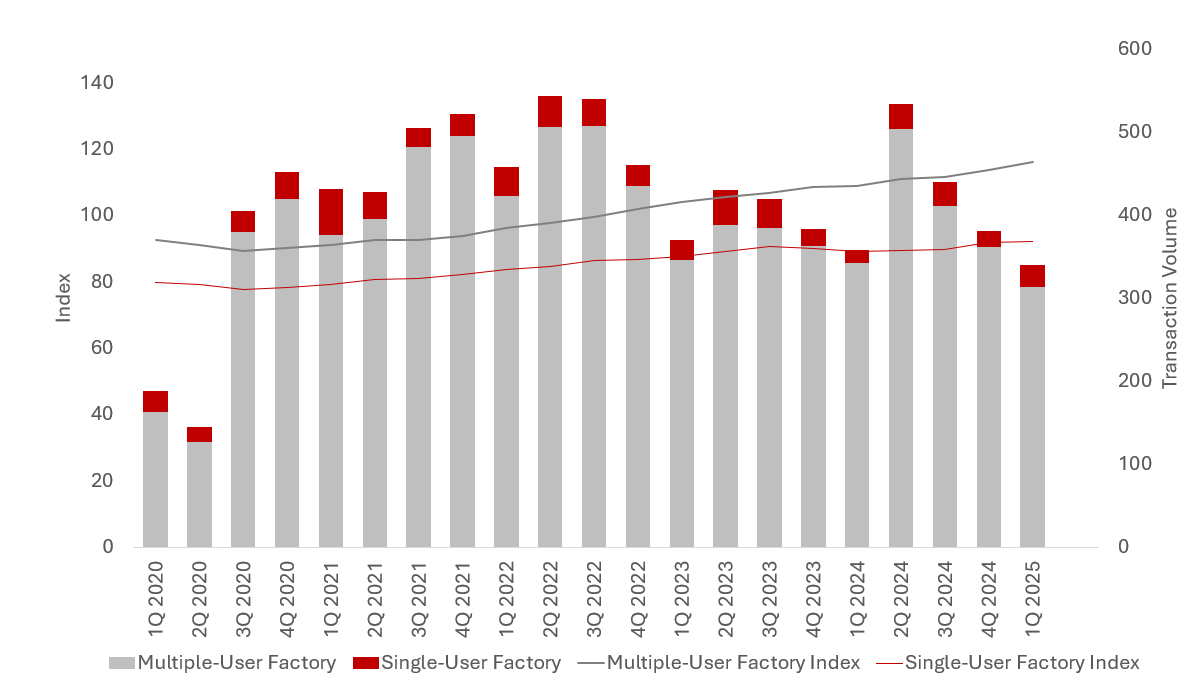

Price and Sales Transaction Volume

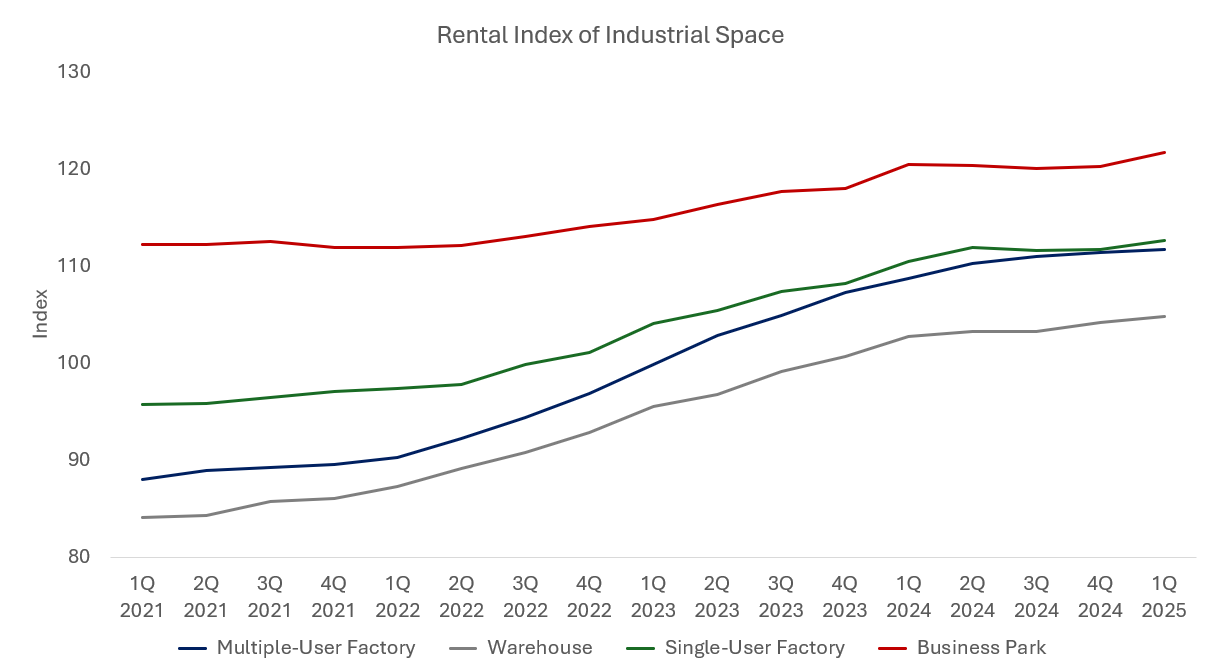

Prices for Multiple and Single-user Factory increased by 1.9% and 0.4% quarter-on-quarter (q-o-q) in 1Q 2025.

In contrast, Multiple-user Factory transaction volume fell by 13.3% q-o-q, marking a third consecutive quarter of decline. Single-user Factory, however, reversed the 34.5% q-o-q decline in 4Q 2024, achieving a rise of 36.8% in 1Q 2025.

CT Pemimpin, a new freehold B1 industrial building, was launched in February 2025. With its practical design, featuring a high floor-to-ceiling height, direct vehicular access, a large circulation area, and units with efficient and open layouts, it ticked most boxes and attracted buyers. Located between Marymount and Bishan MRT Stations, its central location was a big draw. Finding a suitable industrial space with specifications that meet their business needs is not an easy feat for many end users. It managed to sell 89% on launch day and is now fully sold, although no caveats have been lodged as of 24 April 2025.

Chart 4: Price Index and Transaction Volume

Source: URA, ERA Research and Market Intelligence

The most notable transaction in 1Q 2025 occurred on 13 March 2025, when JTC awarded the tender for the industrial site at 23 Lok Yang Way to Soilbuild Group Holdings Ltd for nearly $70.1 million. Additionally, a freehold Multiple-user Factory at 21 New Industrial Road was sold on 5 February 2025 for $62.0 million.

Table 1: Top Five Sales Transactions in 1Q 2025, based on caveats lodged

Source: URA, ERA Research and Market Intelligence; *Rounded up to the nearest year

Leasing and Leasing Volume

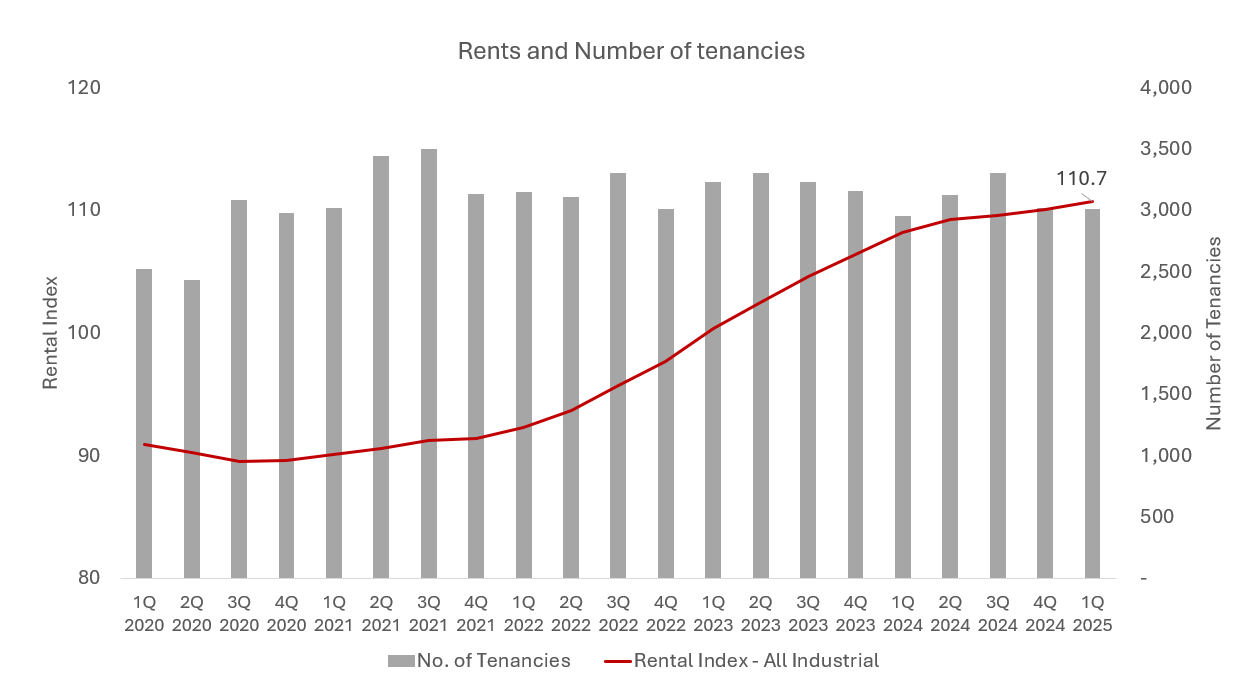

The JTC All Industrial Rental Index continued its upward trend, rising for the eighteenth consecutive quarter in 1Q 2025. Similar to 4Q 2024, rents also grew by 0.5% this quarter. However, despite the marginal increase, rents are likely to plateau and grow at a slower rate. Among all property types, Business Parks rents grew the most this quarter, rising 1.2% q-o-q.

While the rental index has climbed marginally q-o-q, leasing volume has decreased by a slight 0.4% q-o-q to 3,008 tenancies signed in 1Q 2025. This follows a decline in leasing transactions of 8.6% in 4Q 2024.

Chart 5: Rental Index and Number of Tenancies for Industrial Properties

Source: JTC JSpace, ERA Research and Market Intelligence

Chart 6: Rental Index and Number of Tenancies for Industrial Properties

Source: JTC JSpace, ERA Research and Market Intelligence

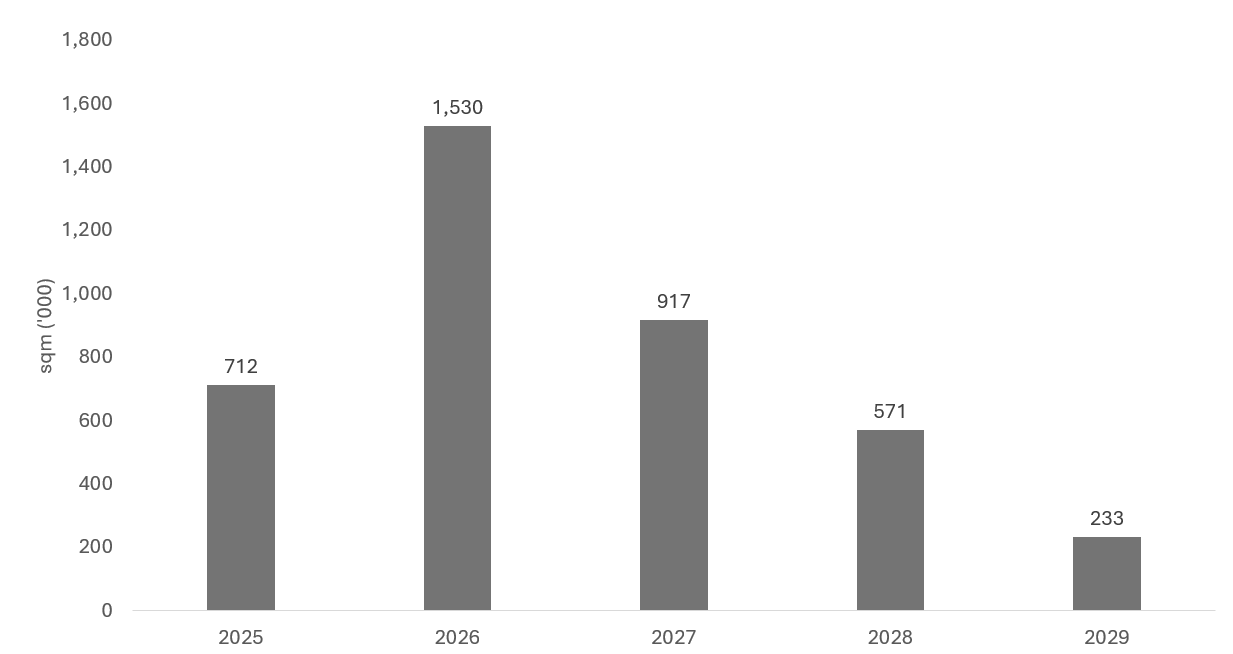

Upcoming Supply

By the end of 2025, JTC forecasts that another 24 new industrial developments will attain their Temporary Occupation Permit (TOP). This will inject an additional 597,000 sqm of industrial space into the market. Some notable developments include a warehouse at DSV Pearl by Logos Pacv SG Propco Pte Ltd in Tukang Innovation Drive (67.700 sqm), a Business Park development in Punggol Digital District by JTC Corporation (72,960 sqm), and JTC Space @ Ang Mo Kio (117,230 sqm). In total, only 264,970 sqm (44.4% of total uncompleted GFA) is developed by JTC.

This slew of completions could cater to the demand for industrial spaces. However, since some of these leases have already been pre-committed, the occupancy rate is likely to remain stable.

New industrial spaces (Multiple-user Factory) developed by the private sector are likely to attract significant attention from business owners looking to purchase their own industrial space.

Following CT Pemimpin’s stellar performance, CT Foodnex and Ecofood@Mandai, both freehold strata food factories, could see renewed interest as well. Despite being located in the north-west of Singapore, they still present opportunities for businesses in the food and beverage (F&B) sector. With many restaurants and eateries across shopping malls and neighbourhood estates, these central kitchens could pique the interest of F&B owners or food caterers.

Chart 7: Supply of Industrial Spaces’ Expected Completion Year

Source: JTC JSpace, ERA Research and Market Intelligence

In conclusion

Protectionist measures between major trade partners such as the US, Canada, and China could cause ripple effects in small and open economies like Singapore. With cautiously optimistic sentiment, we are likely to see more muted growth in industrial rents and prices. However, the extent of growth would be moderated as firms remain cautious about the global geopolitical outlook amid a higher supply of industrial stock with more completions in 2025. Expansion plans could be put on the back burner as businesses navigate the prevailing headwinds.

Furthermore, the slowdown in Fed rate cuts due to persistent inflation rates may lead investors to remain on the sidelines. Transaction numbers might decrease, though not significantly. Due to tighter supply, prices and rents continue to grow at a sustainable pace.

In line with Singapore’s forecasted economic growth projections, prices and rents of industrial properties could see more measured growth, rising by up to 2% y-o-y in 2025.