Following a series of interest rate hikes to combat inflation in 2022 to 2023, the U.S. Federal Reserve may soon ease off on its tightening measures.

According to a poll of economists, the Fed is expected to cut rates come 2H 2024. And as most floating rate mortgage packages take reference to the Singapore Overnight Rate Average (SORA), which in turn tracks the movement of Fed rates, a drop could provide some relief to local borrowers.

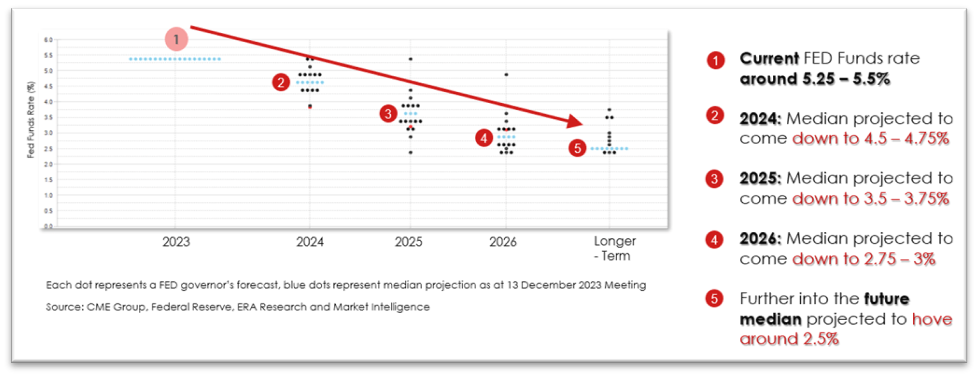

In 2024, the median interest rate is expected to come down from the current range of 5.25% – 5.5% to 4.5% – 4.75%; this range is projected to fall even further over the medium term to 3.5% – 3.75% and 2.75% – 3% in 2025 and 2026 respectively, before settling at approximately 2.5% further into the future.

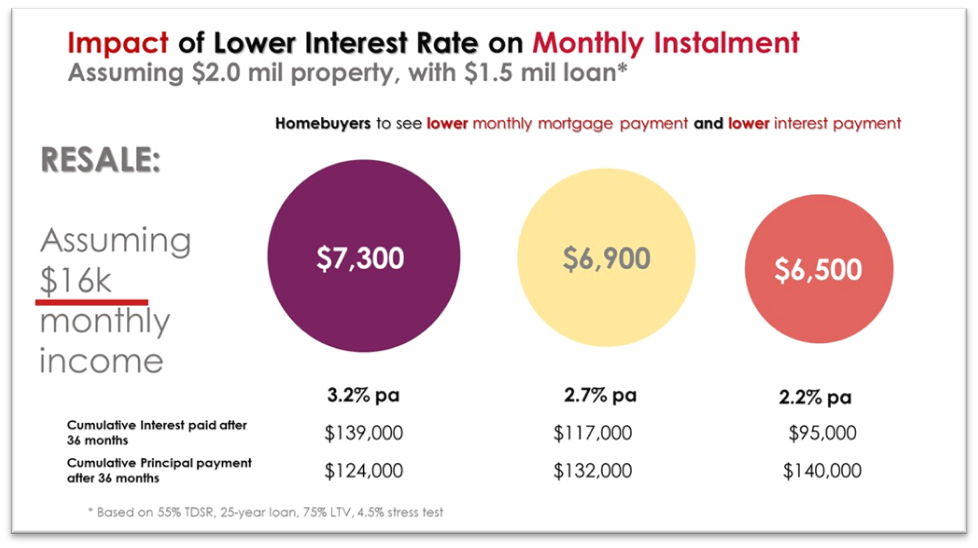

The natural outcome of a reversal in aggressive rate hikes by the Feds is a reduced cost of borrowing, which will almost certainly delight homebuyers in Singapore because of the accompanying reduction in monthly mortgage and interest payments.

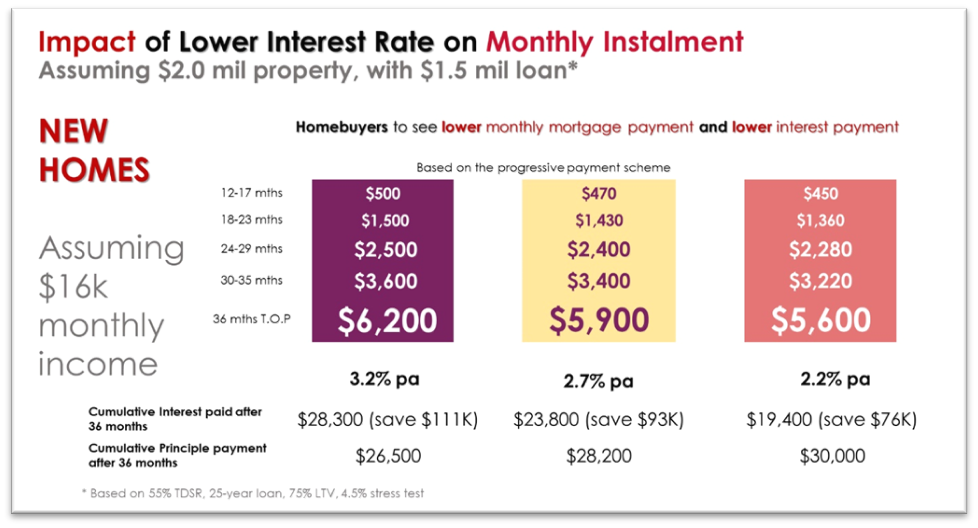

Based on the progressive payment scheme, assuming a couple draws $16K in household income every month, their purchase of a $2M property with a $1.5M loan will result in a $6,200 monthly mortgage payment at a 3.2% pa interest rate. In comparison, should mortgage interest rates fall to 2.2%, they will pay $5,600 (or $600 less) every month than before.

Furthermore, should the variables stay the same, a couple buying a new condo would also be saving more in interest than if they were to purchase a similarly-priced resale private home. For instance, at a 2.2% pa interest rate, the couple would be paying a total of $95,000 in interest after 36 months for a resale private home, but if they were to purchase a new condo, they would end up paying $19,400 in interest, netting them a saving of $76K.

That said, despite the clear benefits that falling interest rates will bring, home buyers may not wish to sit too long on the side lines before acting.

If past market cycles are any indication, we can expect lower interest rates to be accompanied by a rise in demand for local real estate, and consequently, an uptick in new home prices.

When the compounded 3-month SORA begun falling in 2019, it resulted in a market rally from 2020 to 2022, causing new home demand, and more crucially, prices to rise sharply. Between 2Q 2020 to 1Q2022, PSF prices for new homes went up by 25.7%, rising from $1,726 to $2,171.

Therefore, in light of the possibility that history may repeat itself, it may be wiser to buy a home now, rather than later.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers.

For avoidance of doubt, ERA Realty Network and its salespersons accept no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.